By Mark Giammalvo

|

By Mark Giammalvo |

|

|

What would you think if you saw this sign posted in the window of a business? It would get your attention and maybe even a few laughs. Unfortunately, the topic of health care is no laughing matter. Health

care benefits are becoming increasingly important in the struggle to keep

good employees. Are you aware of all your options? It seems like things were

so much simpler just a few years ago. Regarding health care, at one time

most businesses had the same insurance company. You remember: the old 80/20

indemnity plans with the quarterly deductible? The patient paid 20 percent

of the office visit plus the quarterly deductible, and the insurance provider

paid the remaining 80 percent. I don't know if it was good or bad, but it

sure seemed a lot simpler. A major chore

In addition, we enlist the help of a broker who obtains quotes form several different companies each year. Even so, every year I am shocked over our renewal rates. In the past, they have gone from chunky 12 percent to whopping 30 percent increases. These increases are tough to stomach for both the employer and the employees. Currently we pay 50 percent of our employee's health care benefit. Even so, how do you tell your employees every year that their weekly pay just took another $20 hit? How will the business cover a $5,200 annual increase? Let me tell you, it's just not easy. In the end, it comes down to several key issues. At

first blush, the health care market can seem like a labyrinth of nightmares.

There are many companies to choose from and each company has a variety of

plans and configurations. One company will offer a two-tier rate as Single

vs. Family coverages. Other companies will offer three- or four-tier plans

that include the two-person households (Single Plus One). Once you know the

rate, the business and employees can figure their annual costs. That's the

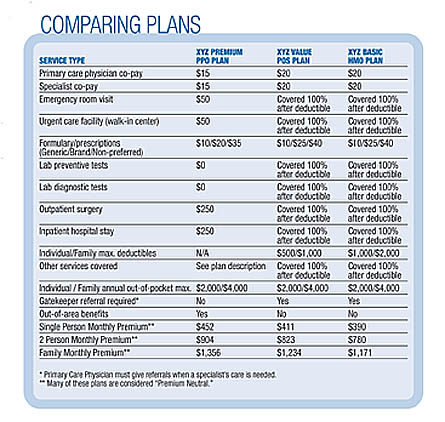

easy part. The hard part is choosing a plan everyone can best live with. What's your style? Will your family have to go to the hospital this year? If so, can you handle the first $2,000 out-of-pocket expenses? Do you and/or your employees require many maintenance prescriptions on a regular basis? Can you handle a formulary (drug) benefit of 10/25/40? It's a lot to think about. Don't be surprised if the insurance company makes you fill out a questionnaire concerning details of how you pay your insurance. A common question on this form is what percentage your business pays toward employee health care. Typically the insurance companies will mandate that the business pay at least half of the family plan's premiums and a third or more of the single plan's premiums. Why would the insurance company care what portion your business pays? It all has to do with the insurance underwriters and how they determine risk ratios. A business that pays for half of the health care benefit will tend to have a better ratio of healthy subscribers. The logic is that more people will sign up because a larger amount is employer paid, and that means more healthy people in the plan. But when the employee has to pay more, those who know they are more likely to need health care coverage will tend to sign up more readily. This is because they have no choice but to purchase the coverage. This ends up costing the insurance company more money. Other questions on the questionnaire may ask about

the number of "eligible" employees that are currently not on the plan. This

normally means other full-time employees who are obtaining health care elsewhere,

such as through their spouse's employment. Again, the insurance company wants

to know about possible future risk. The insurance company knows that they

may be on the hook for providing coverage if an employee's spouse suddenly

loses his or her job or heath care. Unanticipated increases However,

the insurance company decided to slip in an additional rate this year. Even

my health care broker had never heard of it. After choosing our renewal plan

we were stunned when we received our first bill. When I called the representative at the insurance company, he directed me back to my rate quote sheet. Sure enough, down at the bottom, was a statement that said that we had two "Medicare Active Employees." On a subsequent conference call, my insurance broker and I challenged the account representative over this new unannounced rate structure. The account representative had a few interesting explanations. He said that in the past, overall group rates were higher to make up for the "older high-risk" members on Medicare. The insurance company had decided to spread out the risk factor in a more realistic way. Another words, give more premium burden to the Medicare-active members. However, federal law dictates that Medicare is the primary provider when a Medicare active participant is on a plan with 20 members or less. That being said, why would the insurance company charge more if Medicare were the primary responsible provider? The representative's answer was interesting: He said that a person who is on Medicare and still on a private plan is considered a "red flag" with the underwriters. Why? Because underwriting presumes that member must have a high-risk health factor if they need both the Medicare and a private plan. Needless

to say, we did not get very far in the discussion. Our broker believes that

they quietly pushed this new three-tier structure through in hopes of catching

most subscribers off-guard. It would have been nice for them to bring this

change to our attention before we chose the renewal plan. Then we would have

had a truer picture of the coming year's cost. Don't forget details In

addition, the insurance companies can offer incentives to doctors that stay

within the pool amount for the year. Doctors that overutilize care with too

many specialists referrals may not receive the dividend payment. Some patients

and physicians argue that this method reduces the utilization of services

and even compromises patient care. Others counter that the plan is fair and

unbiased. Buyer beware If

you belong to an association, check on whether health care is offered through

that organization. If you are not an automotive association member, visit

the Internet site of the U.S. Small Business Administration (SBA) at

www.sba.gov.

Search for AHP or Association Health Plans. These plans have been proposed

in Congress to allow groups of small businesses to band together to buy health

insurance. According to SBA, some of the projections are that businesses

could save as much as 13 percent on their coverage by taking advantage of

AHPs. The U.S. House of Representatives passed the legislation in 2003, and

the Senate is due to take up the matter next. Arm yourself with data

|